The Third Option in Money and Life

Stuck between two options? Consider whether a simple third option might be your answer for moving forward.

When it comes to solving financial stress, it’s natural to think you have only two options—make more or spend less. While it’s possible one or both will figure into your eventual solution, there’s a third, more doable, and I think exciting option available. And that’s to manage—more happily and realistically—exactly what you already have.

In this article:

- A story: to move or not move?

- What the third option looks like with money

- What intentional money management looks like

- Examples of "third options" in life

- How I help youThe third option: a story

The idea of a third option is true in life as well, as illustrated by the following example. Several years ago, I was beyond ready to move into a nicer place. I had finally paid off all my debt and was ready for an upgrade. You see, for the past 5 years, I’d been making do without a dishwasher, A/C, and most inconveniently, a washer and dryer. (Remind me to tell you sometime about the creeper watching me in the reflection of a washing machine at the laundromat down the street—insert shudder.)

I also had what my brother affectionately called “the African field hospital shower.” This vintage clawfoot bathtub with a circular shower curtain sure looked charming but was drafty. It also dropped around my sister-in-law on one visit, and around me multiple times.

Don’t get me wrong; I had loved where I lived. The landlords, neighbors and neighborhood could not have been nicer, the place itself was cozy and had loads of character, and a best friend lived in a cottage behind me. But I now had significant breathing room in my monthly budget and I was ready for more space and those modern conveniences we’ve come to appreciate.

My options felt like “stay” or “go,” but honestly, I wasn’t finding anywhere I wanted to move. None of the condos or apartments felt worth the corresponding increase in monthly rent. So I did what we all do when trying to decide between two not-great options: I did nothing, except bounce mentally between two and, feeling positively stuck.

But an off-hand question from my dad introduced a third option: “What if you spent some of the money you’d pay for a nicer place and just upgraded your current home?” What a concept—a third option.

Answering that question helped me realize that what I was mostly seeking was even a small upgrade and change, and these could both be accomplished with some simple adjustments. I bought a new couch. It, however, came defective and was too stiff so I ended up returning it. Once I knew I wasn’t stuck with it and could replace it if I chose, I suddenly really appreciated my existing, comfortable couch.

I bought a new coffee table and a rug and some plants in pretty pots and honestly can’t remember what else. I explored the option of a washer and dryer that could be hooked up to the kitchen sink, but decided it wasn’t a big deal to do one more year at the laundromat. Plenty of people in big exotic cities do it for life, so I certainly could manage for one more year.

And I did. Embracing the third option bought me another fabulous year in that beloved space. And instead of spending more monthly money on a higher-rent place I didn’t actually like much, I was able to save aggressively for the first time in my life. This meant I was able to buy a home of my own the next year after a breakup propelled me that direction.

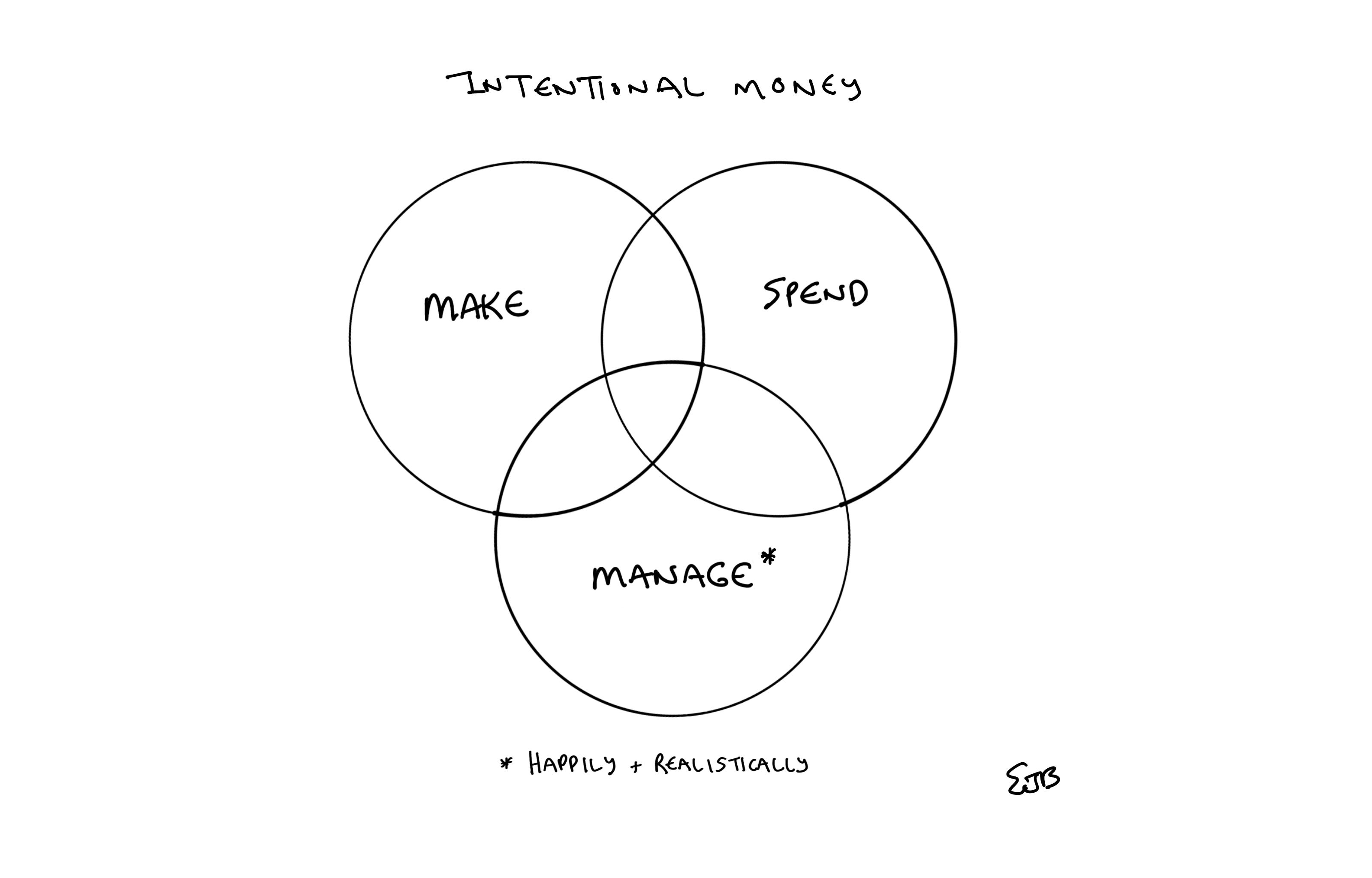

The third option in money

Back to what this has to do with money: When you realize you have choices, you’ll sometimes be surprised by how much more you can make of your existing situation.

Making more money might help your financial situation, but it often doesn’t, thanks to lifestyle creep.

Spending less might help your financial situation, but also often doesn’t since we make unrealistic cuts, or lean on discipline to muscle through. I’ve found that unrealistic discipline has a short shelf-life.

Managing money differently, though. Now this is where the magic is. You may feel like you’ve been trying to manage your money, and it’s demoralizing to feel like your best efforts aren’t getting you the results you want. But have you tried realistic money management? It’s where you accept your financial situation, spending decisions and your current income, instead of wishing you had more money.

Speaking of wishing you had more money, it makes me think of this “Deep Thought” by Jack Handey (of SNL fame):

It’s easy to sit there and say you’d like to have more money. And I guess that’s what I like about it. It’s easy. Just sitting there, rocking back and forth, wanting that money.

It’s in this third option—taking a more intentional approach to managing your money—where you can see that you actually have choice. You can finally see, without judgment or shame, how you might be able to plan your money differently or make minor adjustments to get major results.

What does intentional money management look like?

Have a why. Yes, that sounds super simplistic, but if your situation isn’t bothering you that much or there’s nowhere/nothing specific you want (out of debt, be able to leave your job, have money to invest in a vending machine business, etc), why would you do anything other than what you’re doing now?

Quantify your cost of living. Do this on an average monthly basis, separate from your monthly income. We have a tendency to make our cost of living conveniently “squish” into the box of income by ignoring the occasional expenses, or the ones we feel guilty about.

Quantify the gap between your income and your current cost of living. It’s one thing to know you are outspending your income, and another to know that you are overspending it by $550 per month on average. Quantified “problems” are much easier to solve than vague ones.

Decide if you want to do something about it. Chances are, you will, especially when it feels doable.

Start budgeting for real. I’ve written about it loads on my blog archive at www.emilyburnett.me. You might like these specific articles here and here (a fun one about COVID budgeting.)

A note for those of you who are already entrepreneuring and figuring out how to make money: I’ll be working on an in-depth piece about the logistics of managing your money with the variable income that is entrepreneurship. It is much harder to budget with money you don’t have, but you can avoid going to the other extreme of throwing caution to the wind and spending willy-nilly anticipating income.

Where else there might be a third option:

Job: It may feel like you either have to stay or go. The third option: have a conversation with your boss to get clarity or make adjustments to buy necessary time. Had I left my last job when I thought I was ready and before making all the adjustments I could think of to make it work, I would’ve missed out on some pretty cool benefits and additional savings.

Business: This is an extreme approach, but it may feel like your options are to put up with the clients making your life miserable or quit your business altogether to get a job. But could you have the conversations that need to be had and let your clients know what you won’t tolerate any longer? Cue Tim Ferriss’ first experience with “firing clients”:

The second question is what 20 percent of my activities, of the people I’m involved with, are producing 80 percent of what I don’t want, and you may want to actually eliminate those before anything else. In my particular case, I noticed of those five wholesale customers who were making a huge contribution to my profit, two of them were professional ball breakers. So we’re faced with a dilemma here, and that is they’re contributing quite a bit of money but there was a huge negative carryover. I took their insults, their browbeating, and it carried over into my personal life. Just had a lot of anger and anxiety with me at almost all times because of this, so I fired those two customers, and I would encourage everyone to fire more customers.

The way I did that was I sent them an email, both of them and I said, “Unfortunately it doesn’t seem as though our work styles are compatible. I would love to continue working with you if the following conditions are met. No insults, no profanity. If that’s the case, look forward to working with you. If not, best of luck, take care. Tim Ferriss.” One of them left, never to be heard from again and the other shaped up immediately and was placing twice as much (sic) orders on a monthly basis.

Relationships: It may feel like the only option is to split-up or put-up. But could there be a third option of talking vulnerably about what’s actually going on? Honest conversation might not salvage every relationship, but it’s worth at least exploring that third option for healthier relationships with yourself and others.

Where could the “third option” serve you?

Is there somewhere in your life where you’re bouncing back and forth between what feel like your only two decisions? I dare you to pause, and entertain that there might actually be a third option that opens your next chapter. What’s yours?

If you’re feeling stuck financially in money or life and wanting to be more intentional, I can help. Here’s how:

Making the Most of Payday: This free printable is perfect for you if you’re currently collecting a paycheck, even a fat one. It shows you how to start getting ahead of payday and break-up with that lame paycheck-to-paycheck cycle.

See Your Way to $50K is a no-fluff course helping you create your realistic plan for $50K of financial progress. It walks you through the exact system I created to get out of $50K in debt, build savings, and build my confidence for leaving jobs and taking risks. Completing this quick course also unlocks options for a discounted 1:1 review.

Subscribe to More to Your Life: I’m your risk-taking BFF here to help you live with more peace and create more personal freedom by improving your relationships, money, habits, and work. More to Your Life is a reader-supported publication. To receive new posts, support my work, and be part of the intentional living + intentional money movement consider becoming a free or paid subscriber.